Par Value Method Of Accounting For Treasury Stock

Par Value Method Of Treasury Stock Examples Play Accounting

Treasury Stock Par Value Method Explanation Journal Entries

Treasury Stock Par Value Method Accounting For Repurchase Reissue

Treasury Stock Par Value Method Explanation Journal Entries

Ppt Equity Financing Powerpoint Presentation Free Download Id

Stock Issue Treasury Stock Cost Method Vs Par Value Method T S

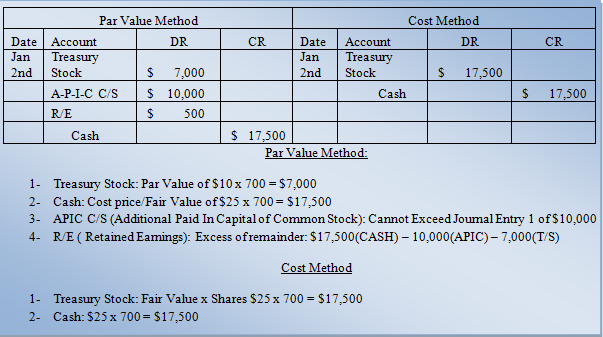

For example if a corporation acquires 100 shares of its stock at 20 each the following entry is made.

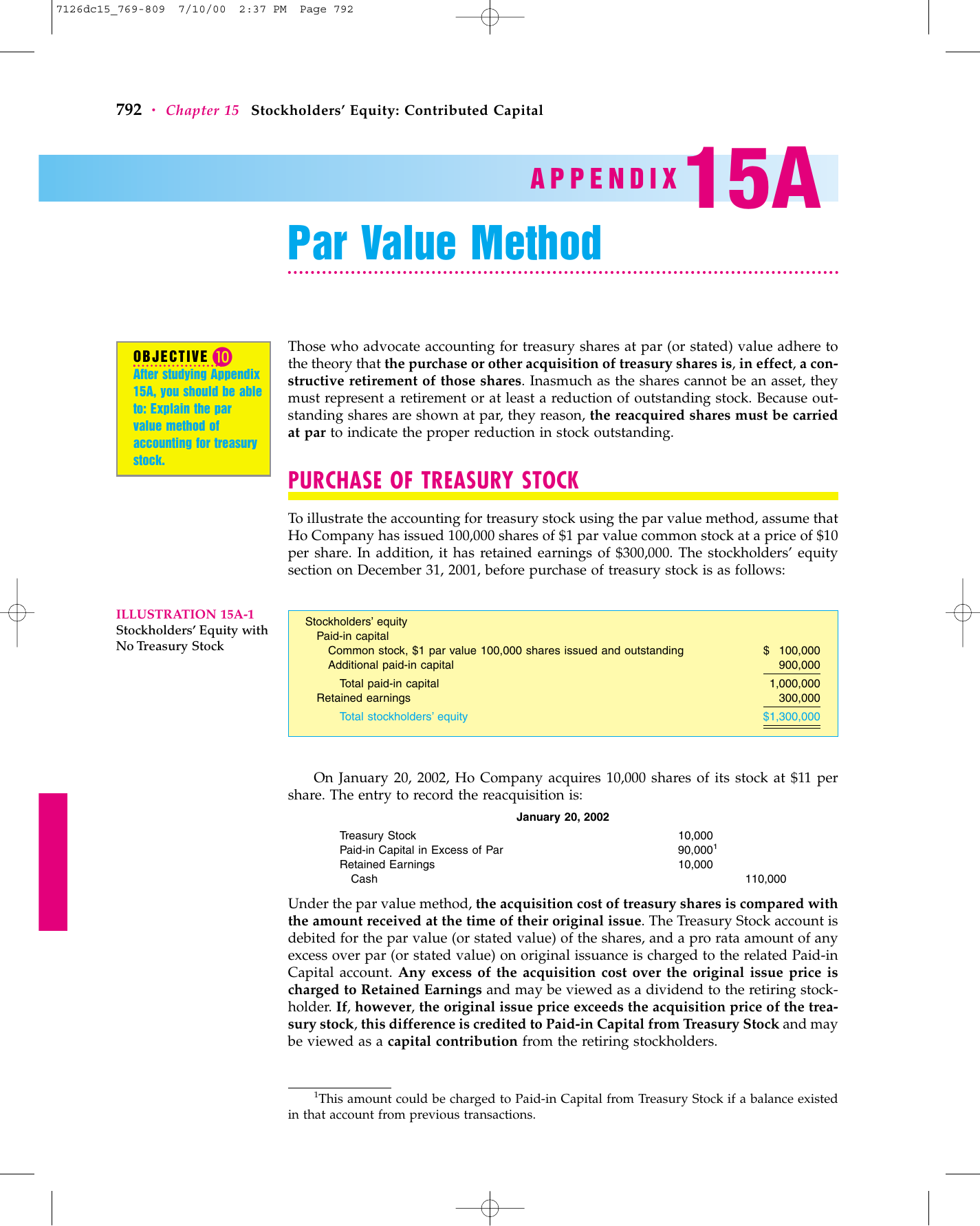

Par value method of accounting for treasury stock. An alternative method of accounting for treasury stock is the constructive retirement method. At the time of acquisition the treasury stock account is debited for the par value of. Since sunny acquired 1 000 shares and reissued 500 shares the. The following discussion explains the accounting treatment of treasury stock using par value method if you want to read about cost method please read treasury stock cost method article.

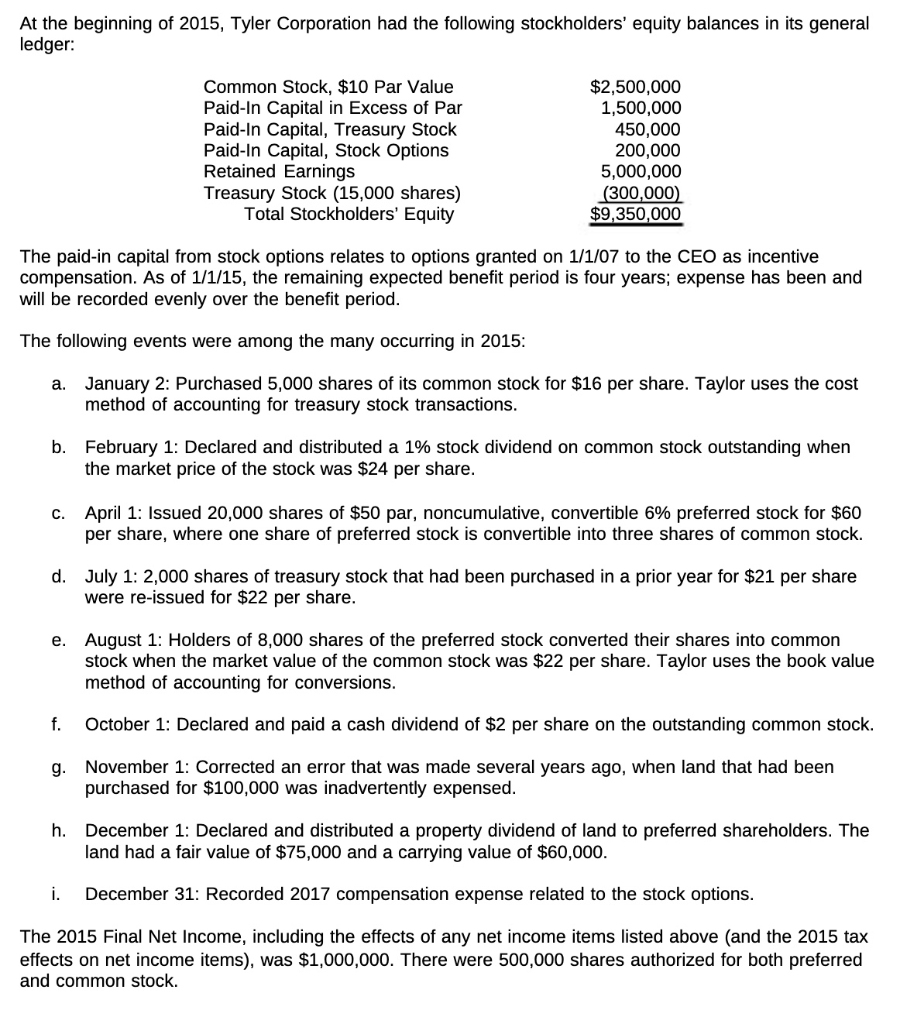

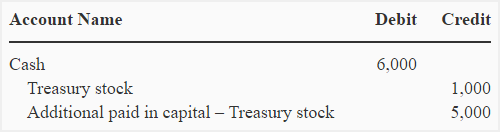

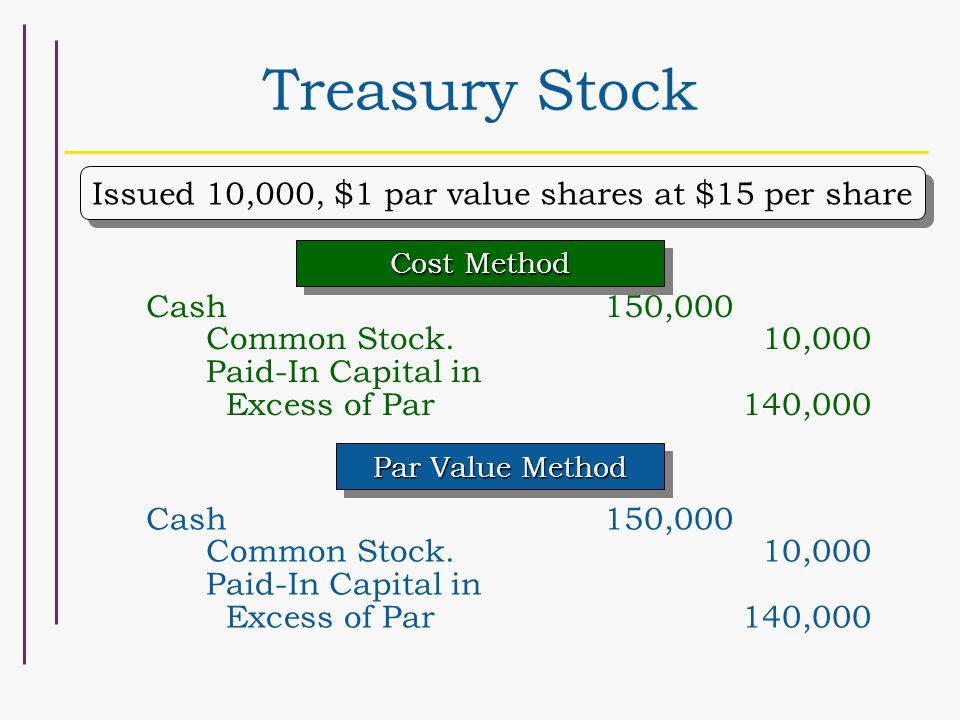

Under par value method purchase of treasury stock is recorded by debiting treasury stock by the total par value of the shares. The board of directors of armadillo industries authorizes the repurchase of 100 000 shares of its stock which has a 1 par value. The transactions relating to purchase and sale of treasury stock are generally accounted for using one of the two methods. Cash account is credited for the actual amount paid to purchase the treasury stock.

Treasury stock refers to shares which have been bought by the issuing company itself. Read morepar value method of treasury stock. The par value method is illustrated in intermediate accounting textbooks under the cost method the cost of the shares acquired is debited to the account treasury stock. These are cost method and par value method.

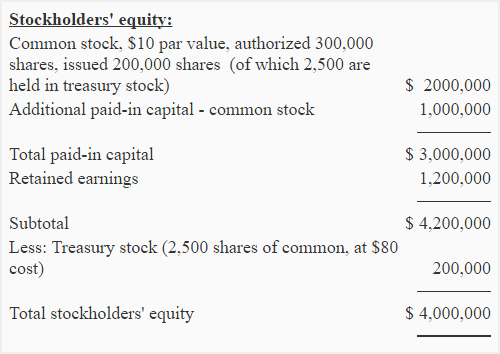

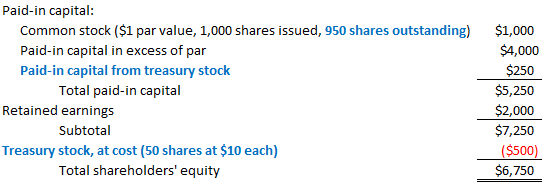

The stockholders equity section equals the same amount as the balance when using the cost method the difference is that the treasury stock balance is deducted directly from the par value of the original stock consistent with the view that acquisition of treasury stock under the par value method is the same as retiring the shares.

Intermediate Accounting Ppt Video Online Download

Treasury Stock Cost Method Explanation Journal Entries

Ppt Components Of Stockholders Equity Powerpoint Presentation

Adequate Disclosure Contra Accounts For Assets Liabilities Equity

Equity Financing Ppt Video Online Download

Par Value Method

How The Sale Of Treasury Stocks Affects Shareholder Equity The

14 2 Analyze And Record Transactions For The Issuance And

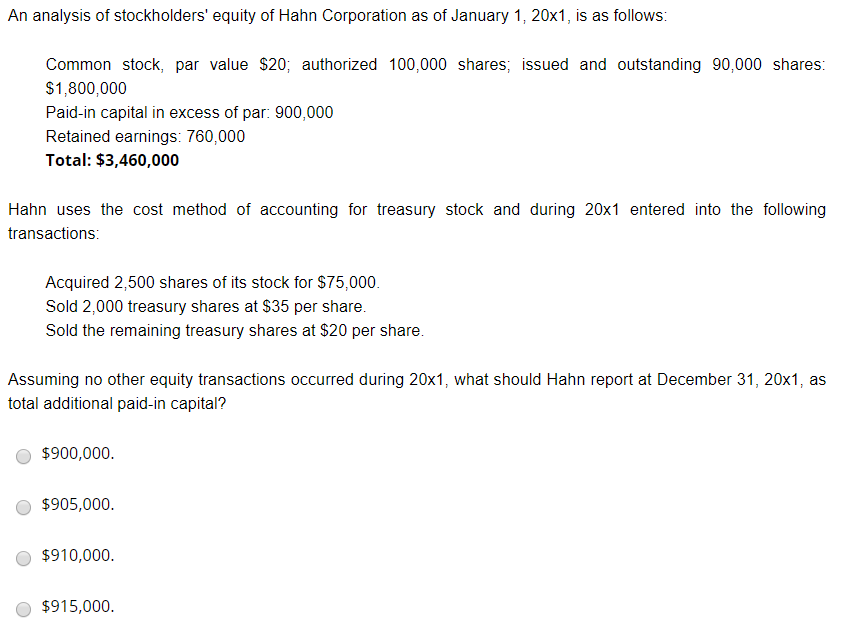

Solved An Analysis Of Stockholders Equity Of Hahn Corpor

How The Sale Of Treasury Stocks Affects Shareholder Equity The

Treasury Stock And Accumulated Other Comprehensive Income

Under The Fair Value Method If An Executive Does Not Exercise A

7 Accounting For Equity